HVAC Insurance: What Every Business Owner Must Have

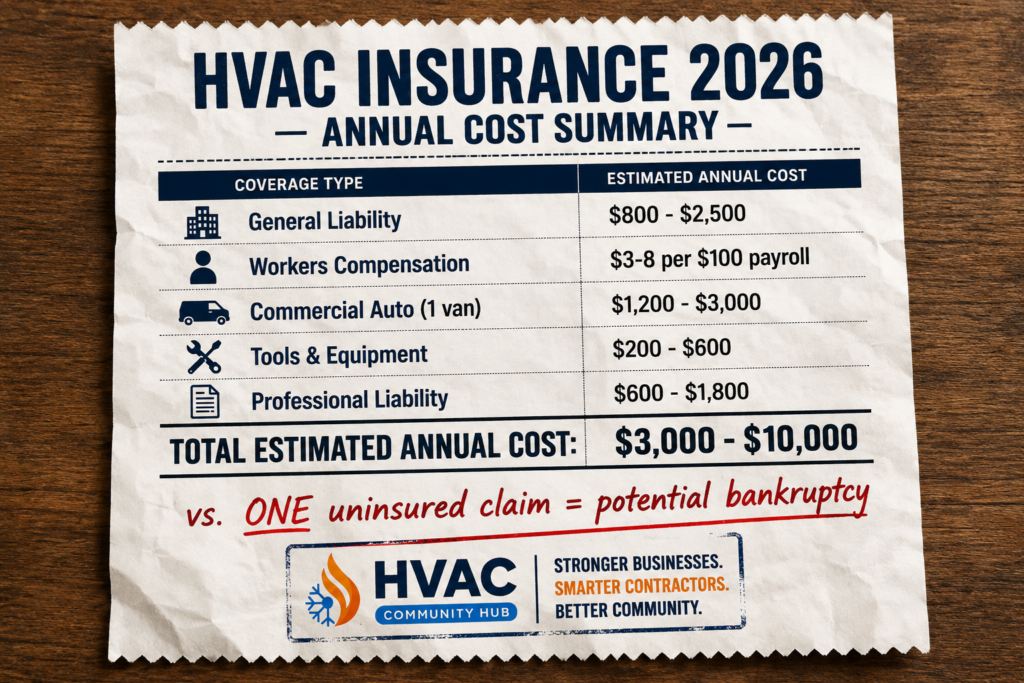

Every HVAC business owner needs the right HVAC insurance in place before anything goes wrong — because when something does go wrong, it can go wrong fast and expensively. A technician installs a furnace that causes a house fire. A worker falls from a roof. A refrigerant leak damages a customer’s property. Without the right coverage, any one of these incidents can bankrupt a business overnight. Furthermore, total annual insurance costs for a small HVAC business typically range from $3,000 to $10,000 — a small price compared to the financial exposure of operating without it. This guide covers exactly which types of HVAC insurance your business needs, what each one covers, what it costs, and how to avoid the most common coverage mistakes.

Why HVAC Insurance Is Not Optional in 2026

HVAC work combines multiple high-risk activities every single day. Technicians work with electricity, handle pressurised refrigerants, use open flames for brazing, and operate on rooftops and in confined spaces like attics and crawlspaces. This risk profile means HVAC businesses face insurance requirements that go well beyond what most other service businesses need.

Furthermore, the consequences of operating without proper insurance are severe. If your general liability or workers compensation policy lapses, your contractor licence can be automatically suspended in most states. Every job you are working on becomes technically unpermitted until you reinstate coverage. One incident without the right coverage can result in a personal lawsuit that takes everything you have built.

What Happens When an Uninsured HVAC Business Gets a Claim

Many HVAC business owners think claims will never happen to them. However, even the most careful and experienced technician can have an accident. A $1 million general liability policy sounds like a lot until a tech installs a furnace that causes a house fire. Between structural damage, temporary housing costs, personal property loss, and potential medical claims, $1 million disappears fast.

Without insurance, that entire cost falls on you personally. Legal defence fees alone can run to tens of thousands of dollars before a case is even resolved. The right HVAC insurance does not just cover the claim — it covers the defence costs, the settlements, and the ongoing business costs while you deal with the situation.

Insurance as a Business Requirement — Not Just a Safety Net

Beyond protection, HVAC insurance is a business requirement in multiple ways. State licensing boards require proof of general liability and workers compensation in most states. Commercial clients require certificates of insurance before allowing contractors on site. Property management companies and real estate agents will not refer work to uninsured contractors.

Furthermore, having the right coverage in place makes your business more attractive to high-value commercial clients who check insurance status before signing contracts. In this way, good HVAC insurance does not just protect your business — it actively helps you win more work.

The 6 Types of HVAC Insurance Every Business Needs

Here is a complete breakdown of the insurance policies every HVAC business should have in 2026 — what each one covers, why you need it, and what it typically costs.

General Liability Insurance — Your Most Important Policy

General liability insurance protects your business when your work causes property damage or personal injury to a third party. It covers legal defence costs, settlements, and judgements against your business. For HVAC businesses, this is the most essential policy you can have.

The recommended coverage amount is $1 million per occurrence and $2 million aggregate — meaning $1 million for any single claim and $2 million total across all claims in a policy year. General liability for a small HVAC business typically costs between $800 and $2,500 per year depending on your revenue, location, and number of employees. Some states require specific minimum amounts for contractor licensing — Texas requires $300,000 to $600,000 and Washington requires $250,000, for example.

Workers Compensation Insurance — Required in Most States

Workers compensation covers medical expenses and lost wages for employees injured on the job. HVAC work is physically demanding and carries a higher-than-average injury risk. Falls from roofs, electrical shocks, burns from brazing equipment, and strains from heavy equipment are all common claims.

Workers compensation is required by law in most states the moment you hire your first employee. Rates typically run $3 to $8 per $100 of payroll depending on your state and claims history. Skipping this coverage is not just risky — it is illegal in most places and can result in significant fines and personal liability for any injured worker’s medical costs. You can learn more about building a safe and well-protected team in our full hiring guide — HVAC HIRING

Commercial Auto Insurance — Essential for Every Work Vehicle

Personal auto insurance policies specifically exclude business use. Any vehicle used for HVAC work — whether it belongs to your business or to an employee using their personal vehicle for work purposes — needs a commercial auto policy.

Commercial auto for a single HVAC service van typically costs $1,200 to $3,000 per year. Fleets of three to five vehicles typically cost $4,000 to $8,000 per year. Coverage should include liability at $500,000 to $1 million combined single limit, collision and comprehensive for your own vehicles, hired and non-owned auto for rental vehicles and employees’ personal vehicles, and cargo coverage to protect tools and equipment inside the vehicle during transit.

Tools and Equipment Insurance — Protect What You Work With

HVAC technicians carry thousands of dollars of specialist tools and equipment. A single van full of HVAC tools can represent $15,000 to $30,000 in equipment value. Tools and equipment insurance covers theft, damage, and loss of your tools whether they are on site, in your van, or at your storage facility.

Keep a current inventory list with serial numbers, photos, and replacement costs for every tool and piece of equipment. Claims without documentation get denied. Tools and equipment coverage typically costs between $200 and $600 per year for a small HVAC business. Without it, a single theft or damage incident can cost your business thousands out of pocket.

Professional Liability Insurance — Essential for Design Work

Professional liability insurance — also known as errors and omissions or E&O insurance — covers claims that your professional advice, design, or recommendations caused a client financial harm. This is particularly important for HVAC businesses that do load calculations, duct design, or equipment selection for commercial clients.

For example, if you spec a commercial HVAC system that a building owner later claims was undersized — causing excessive energy bills — the claim can be brought against you even if you did everything correctly. Legal defence costs alone can run to tens of thousands of dollars. Professional liability insurance typically costs $50 to $150 per month depending on your revenue and the scope of design work you undertake.

Business Owner’s Policy — The Smart Way to Bundle Coverage

A Business Owner’s Policy — commonly called a BOP — bundles general liability, commercial property, and business interruption coverage into a single policy at a 10 to 15% discount compared to buying each policy separately.

Business interruption coverage is a valuable inclusion that many HVAC owners overlook. It replaces lost income if your business cannot operate due to a covered event — a fire, a major theft, or a natural disaster. For a business where every non-working day is lost revenue, this coverage can make the difference between surviving a crisis and closing permanently.

How to Keep Your HVAC Insurance Costs Down

Insurance is a cost of doing business but that does not mean you should overpay. Here are the most effective strategies for managing your premiums without reducing your protection.

Bundle Policies With One Provider

Buying multiple policies from the same insurer almost always produces a discount. The Business Owner’s Policy already bundles three key coverages. Going further and adding commercial auto and tools coverage to the same insurer can produce an additional saving of 5 to 15% across your total premium.

Furthermore, bundling with one provider simplifies your admin. One renewal date, one contact, one certificate of insurance to manage. This reduces the risk of a policy lapsing because a renewal notice was missed among multiple different providers.

Build and Document a Strong Safety Record

Your claims history is one of the biggest factors in determining your insurance premium. Businesses with few or no claims pay significantly less than those with frequent incidents. Investing in safety training, proper equipment maintenance, and documented safety procedures reduces both the risk of claims and the cost of coverage.

Keep records of all safety training, equipment inspections, and incident reports. Insurance providers reward documented safety programmes with lower rates. Furthermore, a clean claims history over three or more years can reduce your premiums by 20 to 30% compared to a business with multiple claims.

Review Your Coverage Every Year

Your business changes over time. New vehicles, new employees, expanded services, and higher revenue all affect both the coverage you need and the premium you pay. Review your policies every year with your broker — not just at renewal — to make sure your coverage reflects your actual business.

Many HVAC owners are either underinsured because their coverage has not kept pace with their growth, or overinsured because they are still carrying coverage for equipment they no longer own. An annual review with a knowledgeable broker keeps your coverage accurate and your costs optimised.

What to Do When You Need to Make a Claim

Knowing how to handle a claim correctly makes a significant difference to the outcome. Here is exactly what to do if an incident occurs on any job.

Document Everything Immediately

The moment an incident occurs, document it thoroughly. Take photos of the damage or injury. Write down exactly what happened, when, where, and who was present. Get contact details from any witnesses. The quality of your claim documentation directly affects how quickly and how fully it is resolved.

Furthermore, do not admit fault at the scene of any incident. Politely acknowledge the situation and advise the customer that your insurance provider will be in contact. Admissions of fault — even well-intentioned ones — can complicate claims significantly.

Notify Your Insurer as Soon as Possible

Contact your insurer on the same day as any significant incident. Most policies require prompt notification as a condition of coverage. Delaying notification — even by a few days — can give an insurer grounds to reduce or deny a claim.

Have your policy numbers and your insurer’s contact details saved in your phone so you can call immediately from any job site. Furthermore, make sure every technician knows the procedure for reporting incidents — they should never try to resolve a customer complaint themselves without involving you and your insurer.

Frequently Asked Questions About HVAC Insurance

Is HVAC insurance legally required?

Yes — in most states and countries. General liability and workers compensation are required by most state licensing boards. Commercial auto is required by law for any vehicle used for business purposes. Operating without required coverage can result in licence suspension, fines, and personal liability. Check your specific state requirements with a licensed insurance broker.

How much does HVAC insurance cost per month?

Total annual costs for a small HVAC business typically run $3,000 to $10,000 — roughly $250 to $833 per month. The exact cost depends on your revenue, number of employees, location, claims history, and types of work you do. Getting quotes from multiple providers is the best way to find competitive rates.

What is the most important HVAC insurance policy?

General liability insurance is the most important policy for any HVAC business. It covers the widest range of incidents — property damage, bodily injury, and legal defence costs — and is required for contractor licensing in most states. If you can only afford one policy, start here.

Do I need insurance if I am a sole trader or solo operator?

Yes. Even as a sole trader, you face the same liability risks as a larger business. One incident without general liability insurance can result in a personal lawsuit that affects your personal assets, not just your business. Furthermore, most commercial clients and property managers will not hire uninsured contractors regardless of business size.

How do I get a certificate of insurance for a client?

Contact your insurance provider and request a Certificate of Insurance — commonly called a COI. Most providers deliver COIs within hours via email. Review the COI to confirm it lists the correct policy limits and that the client or property owner is named as an additional insured if required by the contract.

The Right HVAC Insurance Protects Everything You Have Built

Every HVAC business owner works hard to build their reputation, their team, and their revenue. The right HVAC insurance protects all of it — from the tools in your van to the licence on your wall to the business you have spent years growing.

Take Action This Week

First, review your current coverage against the six types listed in this guide. Are there any gaps? Second, contact your broker and ask specifically about bundling options and whether your current coverage reflects your actual business size and revenue. Third, make sure every technician knows the incident reporting procedure so claims are handled correctly from the first moment.

Furthermore, if you want support building a more protected and professionally run HVAC business — including systems, templates, and a community of HVAC owners sharing what works — HVAC Hub is exactly where to start.

Visit hvachub.co to join free and start building the business your hard work deserves.

Responses